Sprout Social Writeup

Short Thesis: COVID Pull Fwd Brings Tough Growth and CAC Comps for Non-Sticky Application SaaS Player Trading at >13x CY22 Sales

Short Thesis: COVID Pull Fwd Brings Tough Growth and CAC Comps for Non-Sticky Application SaaS Player Trading at >13x CY22 Sales

In short, 2H ARR growth will materially decelerate to below the FY25 guided growth rate as easy comps, low hanging digital transformation fruit, and small business starts cool while company spending is increased to capture the upmarket opportunity leading to slower growth and higher OpEx than the street is expecting. Skip to the Bear Narrative section if you know of the company/don’t want to read dribble on what they do.

Bear Points:

Pull forward from COVID as small and large businesses needed to manage their social presence overnight and “easy” digital transformation projects will lead to difficult net new ARR comps; and, a return to a normalized CAC will pressure growth and margins in 2022 and beyond

Easy to displace product and SMB/Mid-Market focus caps Sprout’s expansion motion/opportunity

To move upmarket Sprout will have to:

Invest heavily in R&D to create feature parity with Sprinklr, other social listening tools, and build out a backend that supports feeding data from Sprout into other enterprise systems

Change their GTM motion to a more costly direct sales force introducing execution risk

Expensive on a relative, growth adjusted, and Rule of 40 adjusted basis vs stickier and higher NDR software names makes for a strong factor short or against other High Growth & No Profit companies

What the Company Does:

Founded in 2010, Sprout Social develops and distributes software for social media management. This includes products for Engagement (monitoring engagements across different social platforms), Publishing (scheduling and delivering content across different social platforms), Analytics (analyzing metrics across social platforms), and Listening (monitoring conversations about your brand/competitors/relevant topics on social media).

In short, a company using Sprout’s software can manage and analyze engagement and content on their brand’s various social accounts (Instagram, Facebook, Twitter, Reddit, etc) from one centralized interface.

Sprout has traditionally sold its software to SMBs via an inbound motion that attracts prospective customers through unpaid content marketing to encourage free trials. Recently, the company has begun its move upmarket. Today, Sprout has over 32,000 customers, with over 692 paying more than $50k annually and one paying over $1mn annually.

The company IPO’d in 2019 at $17/share and currently trades at 18x TTM sales. Annual Recurring Revenue at the end of FY21 was $224mn and Free Cash Flow was $14mn in FY21 (SBC was $22mn).

How the Company Makes Money:

Sprout charges per user per month (an organization that has 20 users on Sprout would pay for all 20 users) with 3 plans ranging from $89/month to $249/month when billed annually. The range of plans include up to 10 social profiles (additional profiles incur monthly charges) and vary in feature set based on the level of reporting, workflows, and integration options they contain. The company’s Listening and Premium Analytics products are an additional monthly charge. In 2021, the average customer spent $7,057 annually ($588/month), up from $4,974 in 2019.

Recent History:

Since going public in 2019, Sprout has made inroads by expanding their product suite in an effort to move upmarket through its Listening and Advanced Analytics products (recent wins include Square and Kraft Heinz and the company counts Atlassian, Shopify, Tumi, IGH, and Subaru as customers), furthering its lead in the SMB market against HootSuite and upstarts (Sprout is known for extremely simple onboarding, a great UX, and strong customer service), and increasing margins considerably (going from -46% to -15% GAAP EBIT margins from FY19 to FY21).

The company has grown ARR from $92mn in FY18 to over $224mn in 2021 while growing customers from 21,000 to over 31,000 through a strong content marketing and product strategy that has led to higher initial contract values and attracted more enterprise customers (the number of customers spending over $10k annually has grown from 1,392 to 4,917). Sprout’s upmarket success has come on the back of their new Listening and Advanced Analytics products released in the year before the IPO. Sprout’s expansion motion, however, is quite weak but improving. The company can expand a contract with either additional seats, its premium solutions (Listening and Advanced Analytics), and additional social profile upsells. The company’s Net Dollar Retention in the 106-110% range (a reading of 110% signals that its customers in the last period spent 10% more this period; this metrics includes customers who churned) is relatively low for a high-multiple B2B software company (70% of Sprout’s new ARR in a period comes from New Land ARR vs a more profitable mix of 50% at other high growth SaaS cos). There are several explanations for this. First, a SMB focus lends itself towards lower expansion rates (see HUBS at 110%, ZEN at 107% ) due to higher churn rates from customers going out of business or cutting costs. Second, bigger customers typically land with all necessary users on the platform, limiting seat upsells. And lastly, many SMBs customers only require one seat as an employee may wear many hats within an organization (see ZEN’s 119% NDR in multi seat orgs vs 107% overall).

Industry & Competition:

The social media management category has seen success recently. As the world shifted digitally overnight, many businesses big and small increasingly found themselves primarily engaging with customers digitally for the first time. The struggle of logging into, switching between, and managing messages and content on several social media platforms can be burdensome for even the smallest local business. Social media management tools such as Sprout aims to solve this. Additionally, over the past several years more and more customer support requests start on social media. For example, users on Twitter may message @AmericanAir to get up-to-date information on a delayed flight. To enable this, a large company like American needs to associate a social media comment, post, or private message with their contact center and CDP software (the social media management category is largely just a consolidator and shipper of data to other applications such as a CRM, Contact Center, or CDP/Data Warehouse; on a separate note, there are strong barriers to entry in social media management that rules out the build vs buy discussion at a larger enterprise since companies such as Sprout and Sprinklr have special access and partnerships with the large social media platforms).

Sprout’s competitors in social media management can be broken down into Suites and Point Solutions and further by SMB vs Enterprise focus.

Suites:

SMB Focused

HootSuite

$300mn in funding; freemium model; 18mn users

Had an early lead in the SMB segment but has lagged behind since; Sprout has a superior interface and tools

Sendible

European SMB focused competitor with 64 employees; priced similarly with similar feature set

Upmarket

Sprinklr (NYSE: CXM)

1,100 customers (80 $1mn+ customers); 117% NDR, Forrester category leader; direct selling model

Better analytics than Sprout and connectors to other enterprise applications

Logos include Alaska Air, Honda, Lululemon, Prada, MGM Resorts, Nestle, PepsiCo

Trades at 5x Fwd Revenue

NTM est growth 25%

NTM Non GAAP EBIT Margins -7%

Khoros

Vista owned; rollup up of Lithium and Spredfast; changed strategy more towards engagement and contact center solutions

Large companies sometimes use a separate social listening software. These software’s search the web, social platforms, comment sections, and forums for relevant information/conversations relating to a brand and provide more robust querying and analytics tools to monitor this information than the integrated suites mentioned above provide. NetBase and Brandwatcher are the two largest players in the space.

Some adjacent solutions such as Gorgias (helpdesk solution) in the SMB segment offer social messaging as part of their solution. Lastly, in the early 2010s some of the larger marketing players such as Salesforce and Adobe made acquisitions in the space but these solutions rarely compete on deals today.

Bear Narrative:

While the company has seen success the last several years, I argue that the go forward growth algorithm and margin targets for FY22 and the FY25 Plan presented at the most recent investor day are overly aggressive given 1) the product and marketing investments/execution required to move upmarket will at best will weigh on near term margins and 2) the company was a clear beneficiary of COVID pull forward which led to a very strong top of funnel and abnormally low customer acquisitions costs - both of which will revert back.

In short, 2H ARR growth will be materially slow as easy comps, low hanging digital transformation fruit, and small business starts cool while spending is increased to capture the upmarket opportunity leading to slower growth and higher OpEx than the street is expecting.

Claim 1: Sprout is “over earning” and benefiting from strong COVID/Digital Transformation pull through

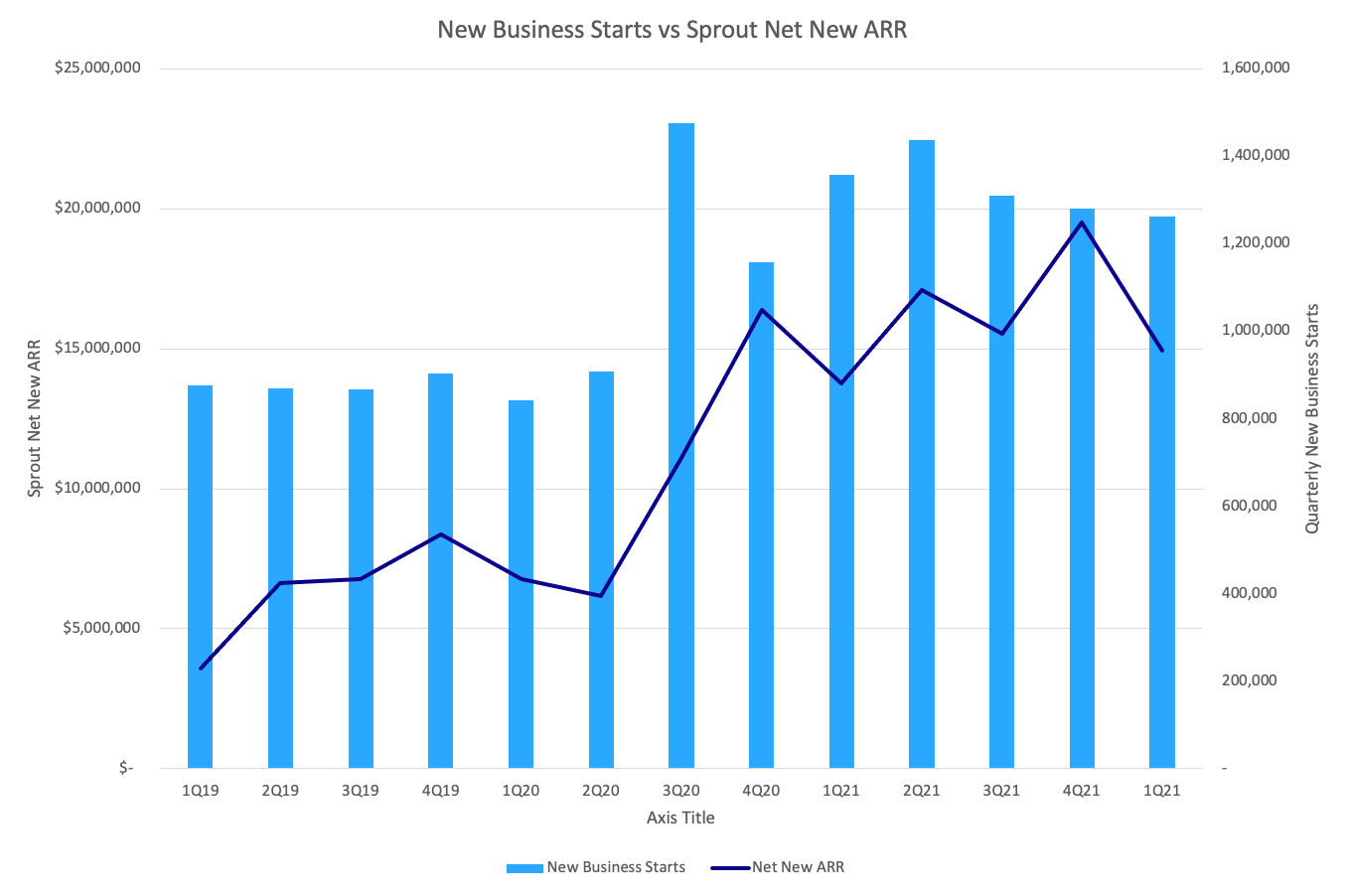

Sprout is a key beneficiary of COVID digital transformation projects and the company will struggle to hit its growth targets in FY22 and beyond. Sprout’s Net New ARR tracks closely with new business starts given the company’s SMB focus and buyer journey. Given this data has trended negative over the past 2 quarters, I believe it is a negative for Sprout’s top of funnel and paints a very ugly picture for the pipeline if it eventually normalizes at pre COVID levels. Furthermore, due to their strong SEO presence and content marketing engine, during the COVID period Sprout won an increasing share of mid market and upmarket logos that typically buy via an account manager outreach but needed a solution quickly. I believe these trends will revert back (i.e. Sprinklr will take back share) and is evidenced by Sprout management commentary noting enterprise buyers discovering Sprout largely through inbound and trial based selling motions.

Going forward, the company will face demand problems as companies that adopted social media management tools during COVID and the subsequent quarters pulled their demand forward to respond to the overnight shift to digital communications (i.e. it will be increasingly difficult for the company to build its pipeline). I believe business starts and website traffic to Sprout’s site are meaningful indicators on near term demand and should be tracked.

Even if Sprout is able to win Net New ARR at similar levels to 2021, I believe there is downside in the stock and for future periods (given management’s 30%+ growth guide through 2025).

For FY22, I contemplate the following scenarios for ARR given various Net Dollar Retention and Net New Land ARR assumptions. For historical context, Net New Land ARR (the ARR Sprout wins from new customers in a given period and calculated as Net New ARR - Net New Expand ARR where Net New ARR is the delta in the provided ARR metric for a given period and Net New Expand ARR is defined as the $ value of Net New ARR attributable to the Net Dollar Retention metric) was $16mn in FY18, $16mn in FY19, $27mn in FY20, and $47mn in FY21.

I model FY22 ending ARR growth at the following levels given a range of NDR assumptions (106%-114%) and New Land ARR ($40mn - $60mn):

In green, I have highlighted the scenarios I find most likely given a tougher demand backdrop and tougher expansion comp.

On the revenue front, this corresponds with ~$252mn in subscription revenue for FY22, in line with guidance given in 1Q22 and sell side but materially below other buy side estimates. Lastly, a decelerating top line throughout the year will pressure the stock.

Claim 2: The pull forward resulted in CAC metrics that will not sustain

Even if Sprout can capture more new ARR in 2022 than it did in 2021, the company will find it challenging to expand margins meaningfully given difficult CAC comps.

Sprout’s Net New ARR (new Lands and Expands) to S&M spend ratio has benefitted from the pull forward in demand. Given the typical buyer’s journey has not meaningfully changed and that improved trial and site conversion metrics alone would not boost revenue at a meaningful level, I believe Sprout’s recent Net New ARR success has been a result of the previously mentioned tailwinds and expect historical CAC ratios to eventually return resulting in some margin deleverage.

I believe Sprout will likely face costs > $1.60 per net new $ of ARR in FY22, closer in line with pre COVID levels.

On the Q4 call, management noted their heavy investments into the S&M and R&D functions for FY22 with the majority of the 40-100bp increase in EBIT margins coming from G&A leverage. With the company guiding towards 33% revenue growth in FY22, I estimate the company will spend $113mn on S&M in 2022 (34% growth y/y) which corresponds with the following costs to land $1 of Net New ARR:

At a minimum, I expect GAAP EBIT loss to increase to -$32mn in FY22, in line with street (in any scenario where CAC is greater than 1.62, this would be higher; 1Q22 was 1.72 for reference).

Lastly, I note the lack of stickiness in social media management software and Sprout’s SMB tilt could pose trouble in a recession as company’s cut non essential spending and ecommerce slows down. Furthermore, given the company’s 21% international exposure (16% EMEA) and recent commentary from other software companies, this offers further downside on macro and forex.

Where I Might Be Wrong:

Upmarket success supports narrative of inflecting NDR and growing TAM

Small biz starts stay elevated and digital transformation projects in the marketing org remain strong

R&D focus on upmarket features makes solution more competitive against Sprinklr and enterprise focused point solutions, leading to increased mid market and upmarket share of new deals and higher starting contract values

Interest rates drive software multiples back above 20x, where Sprout traded pre-correction

Downside & Risk

I believe the stock should trade at a significant discount to other software comps, especially those in the high growth space with 120%+ NDRs and an upmarket focus. Below are the MarTech Tools and Low NDR comps:

I believe a sub 8x multiple on forward subscription revenue is a fairer multiple which implies $39/share.

The following matrix of multiples (4x-15x) and ARR (resulting ARR from the aforementioned scenarios) represent our view on the downside/upside at $65/share:

Again, I believe this is a strong factor short or short against other software names with similar growth rates and FCF margins.

Great write-up! Do you think a potential near-term catalyst could be CY'23 budget resets/cuts in social media/marketing spend? Not sure if IT specifically carves out budget for this type of software or is it more lumped in with marketing budgets? SMB-focused names have shown strength last few q's where enterprise has been more proactive in cutting back early, so wondering if you think that SMB strength is really just the segment lagging enterprise? Also, any thoughts on why they are trading commanding a significant premium to peers? Seems like mostly LOs that own the name - surprised not retail driven.